Blended Retirement System, 101

By Debbie Gregory.

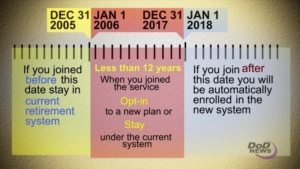

As of January, 2018, the military retirement system as we know it will cease to exist. Instead, service members who joined after 2006 but before January 1, 2018 will have to choose whether to stay with the existing system or opt into the new Blended Retirement System (BRS.)

Those who enter military service on or after January 1, 2018, have no choice; the BRS will be their retirement plan. Another group with no choice is members with 12 or more years of service by Dec. 31, 2017. They will be grandfathered under current High-3 retirement.

More than 740,000 currently serving active-duty members and 176,000 drilling Reserve and National Guard personnel are expected to opt in to the new system.

The new system has three elements: a 401(k)-style component with Defense Department matching funds for entry-level and other service members, a mid-career continuity bonus, and a retirement annuity similar to the one now in place for service members that complete twenty or more years of eligible service.

The new plan combines an immediate but also smaller annuity after 20 or more years of service with a Thrift Savings Plan enhanced by government matching of member contributions of up to 4 percent of basic pay, plus an automatic 1 percent government contribution for all BRS participants, whether they contribute or not to a TSP.

This 401(k)-like nest egg toward retirement is a portable benefit on leaving military service. Veterans can roll the account into an employer 401(k) or continue to make contributions regardless of how many years they served in the military. Because this feature will benefit the great majority of members who leave service short of retirement eligibility at 20 years, the blended plan is expected to be a popular option, particularly with younger servicemembers on their first or second enlistment and officers completing initial service obligation.

Committed careerists, however, are likely to stick with High-3 retirement, which will pay 20 percent more in lifetime annuities if full careers are a realistic goal.

The blended plan has two other features High-3 doesn’t.

By current law, BRS participants are to receive a one-time “continuation payment” at the 12-year mark that, at a minimum, must equal 2½ months of basic pay for active-duty members who agree to serve four more years or one-half month of active pay for reserve component personnel who make the same deal.

The other key feature of the BRS allows those who reach retirement to receive in a lump sum 25 percent or 50 percent of their pre-old-age retirement annuities. In other words, here would be cash to help buy a home, start a business or pay off debts in return for reducing military annuities by one-quarter or one-half until age 67.

Military Connection salutes and proudly serves veterans and service members in the Army, Navy, Air Force, Marines, Coast Guard, Guard and Reserve, and their families.